Research | Policy Briefs

Inflation Reduction Act of 2022

48C

48C Qualifying Advanced Energy Project Credit

(IRA Section 13501)

Background

The Qualifying Advanced Energy Project Credit (48C) program was established by the American Recovery and Reinvestment Act of 2009 and expanded with a $10 billion investment under the Inflation Reduction Act of 2022. The Advanced Energy Project Credit provides a tax credit for investments in advanced energy projects, as defined in 26 USC § 48C(c)(1). (source)

What is it?

The 48C investment credit (IRA Section 13501) offers a 6% credit off a taxpayer’s qualifying investment in an ‘advanced energy project,’ defined as a project that:

Re-equips, expands, or establishes an industrial or manufacturing facility for the production or recycling of a range of clean energy equipment and vehicles;

Re-equips an industrial or manufacturing facility with equipment designed to reduce greenhouse gas emissions by at least 20%; or

Re-equips, expands, or establishes an industrial facility for the processing, refining, or recycling of critical materials

What types of projects/businesses are eligible?

Examples of eligible projects include those that re-equip, expand, or establish facilities that produce or recycle:

renewable energy generating technology;

fuel cells, microturbines, or energy storage systems and components;

carbon capture, utilization, and storage technology;

EV or fuel cell vehicles or components;

grid modernization equipment or components;

energy conservation/efficiency technology;

greenhouse gas emission-reducing technology; or

critical minerals.

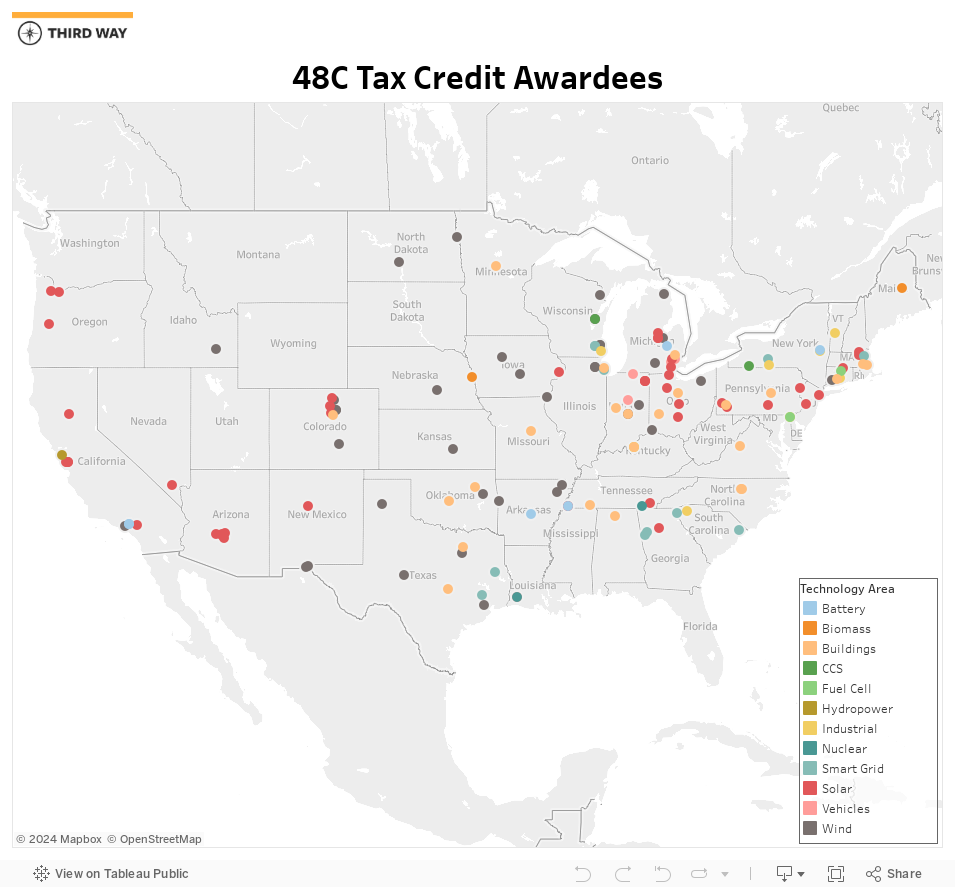

As the IRA allocation is an extension and modification of the 48C credit enacted in 2009 and allocated over two rounds between 2009 and 2013, there are over 150 examples of projects across at least 43 states that have already benefited from the credits. These projects range from factories to produce solar cells or components for solar cells to electric vehicle assembly plants and facilities to manufacture wind turbine gears.

These examples provide a small snapshot of the types of projects eligible for the 48C credit.

According to the IRS, projects most likely to be selected are those that:

Will provide the greatest domestic job creation

Will provide the greatest net impact in avoiding or reducing pollutants or greenhouse gases

Have the greatest potential for technological and commercial deployment

Have the lowest levelized cost of generated or stored energy, or of measured reduction in energy consumption of GHG emission (based on the full supply chain)

Have the shortest project time from certification to completion

Businesses can claim a total 30% credit for projects meeting prevailing wage and apprenticeship requirements.

How do businesses take advantage of it?

The 48C tax credit is available to businesses that submit proposed projects through the Department of Energy’s (DOE) exCHANGE portal. Proposals must be endorsed by DOE before moving on to the IRS.

The Round 1 deadline for concept papers was August 23, 2023, and the full application deadline is TBD. The IRS is expected to make Round 1 allocation decisions by March 31, 2024, after which a second round will be opened. Businesses can access $10 billion worth of allocations, with $4 billion reserved for projects in energy communities with closed coal plants and mines. The tax credit is transferable and will be available until the total allocations run out. Tax-exempt organizations can receive the credit as direct pay.

The DOE’s June 30, 2023 informational applicant webinar on the 48C credit also provides helpful information for submitting a competitive application.

Will the government be sending out future additional guidance?

Only $4 billion ($1.6 billion for projects in certain energy communities) of the total $10 billion will be allocated in Round 1. Businesses can likely expect another funding round to be announced at a later date.

What other IRA incentives are available for clean energy projects?

There is some overlap in eligibility between the 48C ITC and 45X Advanced Manufacturing PTC, which offers tax credits for certain components for clean energy technologies. However, taxpayers cannot stack both tax credits for products produced in the same facility.

Key differentiating factors of 45X are that it

does not require a competitive application process and

is based on costs after components are sold (rather than built).

While the benefits of the 45X credit are less immediate than those of the 48C, the lifetime value of the credit is typically higher (and also not limited to the initial federal government award, as is the case with the 48C credit).

In addition to 45X, other credits specific to the production of certain technologies—such as the 45Q credit for CCS and 45V credit for hydrogen—are also available, while other IRA allocations—such as the $500 million to DOE for enhanced use of the Defense Production Act and $15.5 billion in funding and loans to retrofit automotive manufacturing facilities—provide additional incentives for clean energy technology and facilities.

Funding opportunities offered through the Infrastructure Investment and Jobs Act (for battery materials processing) and CHIPS and Science Act (for semiconductor manufacturing) likewise complement tax credits and programs offered through the IRA.

Additional Resources

48c exCHANGE portal (U.S. Dept of Energy)

Guidance updates on 48C (IRS)